Business of Payments - March 2025

How Paytech makes money

The Payments Business

Full year results from the leading payments processors showed very mixed fortunes: newer players with modern platforms prospered, established businesses struggled.

Stripe led the way with a 40% increase in volume during 2024 to $1.4 trillion and a secondary share sale at a whopping $90bn valuation. Stripe’s management says the company is profitable although released no figures. There are are still no plans to IPO.

One reason for Stripe’s good performance is its success in recruiting AI start-ups as customers. Subscription-based AI services are growing even faster than software-as-a-service vendors did a few years ago.

Figure 1 Source: Stripe Shareholder Letter 2024

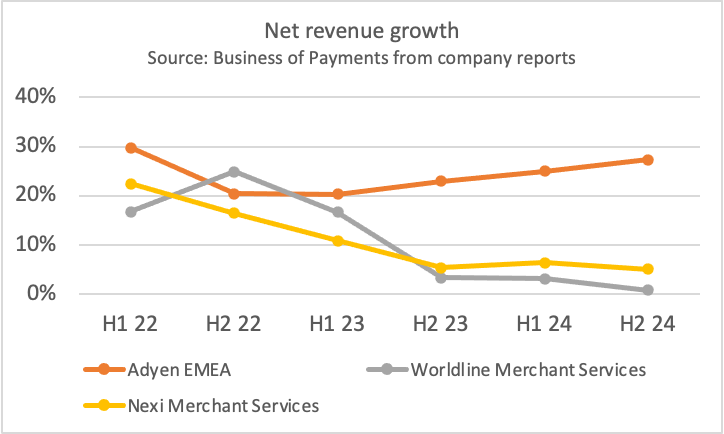

Adyen also reported an excellent 2024. Net revenue was up 23% to €2bn and EBITDA margins remain impressively close to 50%. Adyen’s customer metrics are also strongly positive, with continued growth in the number of merchants processing across channels and in multiple geographies. This healthy performance contrasts with stagnation at Worldline and Nexi. The two traditional European payment champions are struggling with competition from Adyen in enterprise, Stripe in digital and Flatpay, myPOS, SumUp and others in the small business sector.

With shares in both Worldline and Nexi near record lows, investment bankers have been pitching ideas for a merger. Combining the businesses could certainly deliver cost savings although the ensuing disruption would make fixing the product gaps even harder. The Italian government is not keen on the idea and reportedly favours a private equity solution for Nexi.

Despite revenue falling 1% in H2 2024, Worldline reassured investors with news that its JV with ANZ in Australia is growing again and that the JV with Credit Agricole in France will go live in Q2 of this year.

Shift4 is fast becoming a major player in Europe and made a bold move into retail with the $2.5bn acquisition of Global Blue, number one in tax-free shopping. I travelled to Las Vegas for the Shift4 investor day and came away very impressed with both Shift4’s strategy and its people. The equity analysts were less excited. Worried about 2025 guidance and the transition to a new CEO, they marked the shares down 25%. Read my full report on the Business of Payments blog.

In corporate news, Paysafe revealed it had received more than one takeover offer following results showing revenue up just 1% in Q4 2024. It’s easy to see why private equity might be interested as the share a very cheap. Paysafe went public in 2020 at a value of $9b but its current market capitalisation is just $1.4bn. That’s very low for $130bn of payment volume.

Arif Babayev & Nurlan Zhagiparov, co-founders of London-based DNA Payments Group, have made a big move into Austria. The two former bankers have bought 75% of Card Complete and promise to bring much needed modernisation to the business. Card Complete has 1m cardholders, 30,000 merchant customers and processes c.€10bn, roughly 20% of the Austrian acquiring market. It's a daring move. Card Complete is losing money and badly needs investment.

Barclays is reportedly close to offloading its merchant services division (the second largest acquirer in the UK) into a joint-venture with Brookfield, the giant Canadian asset manager. Barclaycard Payments has been struggling for some time with antiquated products, slow decision making and a decaying distribution strategy. Barclays has been trying to sell the division but failed to find a buyer. Instead, the bank will inject £650m into Barclaycard before selling 10% to Brookfield. The Canadians, who also own Network International, would have an option to buy a further 80% of Barclaycard after three years.

The first rule of JV’s is to always be the majority shareholder as JP Morgan’s unhappy relationship with Viva demonstrates. The Information reports that the giant US bank has been looking for an exit. JPM reportedly offered to sell its half its minority 48.5% stake for just $175m, a 50% discount on its original investment. Meanwhile Viva’s CEO has filed an injunction against JP Morgan to block any further lawsuits.

Whatever its future ownership, Viva is not slowing down. Modestly describing itself as “Europe’s first acquirer,” Viva has bought fiskaltrust, a business generating fiscal and/or VAT receipts at over 100,000 points of sale in Austria, Germany, France, Italy, Spain, Portugal and Greece. The companies demonstrated a joint solution at the EUROCIS which uses QR codes. Slicker solutions are available.

Market Pay, the acquirer spun out of Carrefour, has expanded into Denmark with the acquisition of AltaPay, a Copenhagen based PSP. Altapay is an ISO for Elavon Europe and manages >€3bn volume from 400 merchants trading in-store and online. Although Altapay has struggled in recent years (recording just €0.3m EBITDA in 2023) blaming macroeconomic conditions and a "cleanse" of its merchant, this is a good move from Market Pay. The French group gains a springboard into Denmark including a partnership with Danske Bank as well as integrations to Microsoft's in-store software.

MyPOS is making a move into Germany with the acquisition of Lavego, a Munich-based network operator specialising in unattended applications such as vending and petrol. The merger will give myPOS a very useful direct connection to Giro, the German debit scheme. Lavego, which generated sales of €7m in 2023, tried to sell itself to Unzer in 2020 but the deal was blocked by the German regulator.

Capital growth

We’re seeing a steady flow of small fundraises that highlight what’s hot in European payments.

Hands In, based in London, has raised £1m. The business helps shoppers spread payments for high ticket items such as holidays between friends and family members. Hands In won the innovation contest at MPE in 2023 and has Air Europa, the Spanish airline, as a marquee customer. Air Europa says it has generated over €3.8m in incremental revenue through the service.

Receipts, an Oslo-based business that sends digital receipts from POS systems to banking apps through card linking, has raised €1.7m. It’s a tough proposition to get right. Flux, a UK start-up that did much the same thing raised £9m but entered liquidation last year owing its creditors £8m.

Orain Technologies, a Barcelona HQ’d vending payments hardware and loyalty vendor, has raised €6m. The investment will fund expansion into new markets in Europe and Latin America. Competition is fierce in vending with Nayax, NMI and others. Orain, which claims over 1,000 merchant customers, will now use Visa Acceptance Solutions (Cybersource) as its payment gateway.

Urban Fox, based in Dublin and one of Techstars 2019 cohort, has raised €8m for its anti-fraud product that protects against complex synthetic attacks.

Scheming

A new report from Denmark’s central bank brought yet more bad news for Dankort, the local debit scheme which is owned by Nexi. With high fixed costs and declining volumes (see chart below), is Dankort entering a doom spiral? The Danish network’s average cost per transaction is now higher than international cards at DKR2.9 (€0.39) vs €2.3 (€0.31).

Figure 2 Source: Denmark Central Bank

Germany’s Giro scheme is in much better shape but disappointed with 2024 payment volumes growing just 1% to €307bn.

Blik is in fine form. Poland’s mobile payment standard reported a storming performance in 2024 with total volume growing 37% to €83bn. Contactless payments at POS, where Blik works by generating a virtual Mastercard, more than doubled to €2.8bn. Blik has expanded to Slovakia and launching in Romania soon.

Turning to Italy, Bancomat’s new private equity owners backed their growth strategy with the acquisition of Flowpay, an open banking specialist. Flowpay, based in Florence, should not be confused with the Czech Flowpay which provides merchant cash advance.

Elsewhere in Italy, Satispay, a payment and meal voucher app, has raised a further €60m at a self-declared unicorn valuation. Total capital now exceeds a remarkable €500m. Local commentators are not impressed with 2024 financials of €45m losses on just €45m revenue. Impatient investors may have demanded an early move to profitability. Satispay has shocked its merchants by introducing transaction fees for the first time. These are 1% for POS and 1.5% + 20c for eCommerce transactions.

Two into one

The UK’s Payment Systems Regulator has documented how the schemes took advantage of the Interchange cuts mandated by the EU in 2016 to increase their own fees. Between 2017 and 2023, Visa and Mastercard raised their dues and assessments by 25% ahead of inflation. The PSR says having only two schemes is anti-competitive and costs UK business £170m extra each year.

The schemes won’t be unduly worried about the PSR’s proposed light touch remedies: new obligations on Mastercard and Visa to explain, consult on and/or document the reasons for price changes and to provide more detailed financial information to the PSR going forward. Dues and assessment will keep going up.

While the PSR has concluded that having two payment schemes is too few, the British government has concluded that having two regulators is one too many.

Farewell then, Payment Systems Regulator which is to be merged in with the, much larger, Financial Conduct Authority. As one official observed "No other major economy has a standalone payments regulator like this, and it is hard to make the case for it continuing to exist." It seems that the PSR paid the price for its clumsy handling of account push-payment fraud which left the regulator few friends in the industry.

ISV

As businesses increasingly favour buying payment acceptance as an integral part of their point of sale software, payment companies need to make themselves more attractive to ISVs, now often referred to as “platforms.”

Yanvin, based in Paris, is the latest PSP to offer a platforms proposition with the hope of expanding its distribution. As an alternative strategy, some processors are looking to lock-down distribution through acquiring software companies instead. For example, Sipay, based in Madrid, has bought Pikotea, a restaurant specialist based in Cadiz.

ISVs are moving in the other direction. They are increasingly likely to build payments into a vertically integrated stack such as this one from POSbistro, a Polish vendor. The proposition includes restaurant software, payment acceptance via PeP (Nexi) and fiscal printing all running on one, portable, Sunmi device.

While payment bundling is commonplace for small business-focused vendors, it’s a more difficult proposition for enterprise software vendors to get right. Their customers often like to buy components separately to get the best possible deal.

So it’s interesting to see NCR Voyix, whose software powers the largest retailers and restaurant chains around the world, hire a new management team from the payment world. NCR has recruited Jim Kelly (ex EVO and Global Payments) as CEO, Benny Tadele (ex ACI) as EVP Restaurants and Darren Wilson (ex EVO and Gobal Payments) as EVP Retail. Jeffrey Sloan, the former Global Payments CEO, has joined the board. The team’s first move is a deal with Worldpay to sell a combined cloud-based payment/software proposition to retailers and restaurants. New revenue streams are much needed. NCR’s sales to retailers fell 10% in 2024 .

New shopping

Large retailers have a mixed views on autonomous stores. Sainsburys has ditched Amazon’s Just Walk Out technology after a lengthy four year pilot in London. Customers were confused and typically preferred to use more conventional checkout options.

Autonomous technology may be more appropriate for unmanned locations where it can transform empty spaces into walk-in vending machines. In Germany, Reckon is powering a series of small-format Rewe convenience stores at railway stations and EV charging points, locations where conventional stores wouldn’t be viable.

One of the problems with self-checkout is that shoppers regularly steal the merchandise. Tesco has had enough and introduced scales to check that trolleys with self-scanned shopping are the correct weight. Customers are not impressed. “Am I at border control or Tesco?' one asked.

Smartcarts may be a good compromise between full autonomy and the pain of self-scanning. In France, Intermarche is testing devices from Shopic equipped with sensors that automatically scan products into the trolly. Shoppers pay on standard payment terminals at the end of their visit.

In biometric news, three of South Korea’s largest convenience store chains are implementing a face-based payment system called Toss Face Pay. The branding may need some work if it comes to English speaking markets.

Special agents

AI search is becoming increasingly common. A British politician was ridiculed for revealing he had asked ChatGPT “What would be the best podcasts for me to appear on to reach a wide audience that’s appropriate for my ministerial responsibilities?”

Joking aside, this is a serious issue for payments. As people get used to asking AI to research and select products, it’s a small step to asking AI to act on your behalf to confirm transactions and buy stuff for you. And as merchants start employing AI agents to sell their products, shoppers will want autonomous wallets to negotiate their side of the deal.

Agent commerce is likely to be one of the next hot topics. Here are some good examples such as ordering ingredients for dinner from a photo and recipe. It’s like that such agent to agent commerce will need a new set of tools and, according to Simon Taylor, could spell the death of the checkout page as we know it.

SoftPOS

SoftPOS volumes are growing quickly although from a very low base. Visa got plenty of press coverage for saying the value of SoftPOS transaction had tripled in 2024 although didn’t release any numbers. Worldline told investors that it is processing just €13m per month through its “tap on mobile” product although volumes are “growing fast.” Nobody is going to get rich yet.

Poland has been a successful market for SoftPOS with over 50,000 terminals live already. Cashless.pl has found nine solutions on the market and published a helpful summary of the features offered by each one.

Initially, SoftPOS was viewed as a largely micro-merchant proposition but we’re seeing plenty of enterprise deployments.

Shoe shops have been among the early adopters in retail. Rubean has deployed its SoftPOS at Deichmann, the German footwear retailer where it runs on Zebra handhelds integrated with Gebit POS software. Deichmann has even built a special mobile checkout trolley which includes a security tag deactivator and additional items to sell such as shoe polish.

Viva has implemented its SoftPOS solution at Cosmos Sport, in Greece.

Openbanking

What happens if Trump 2.0 instructs Visa and Mastercard to turn off a particular merchant or country that the new administration does not approve of? At a time of geopolitical instability, open banking offers a platform to build consumer payment rails that are independent from American influence or pressure. PSE Consulting look at what needs to be done. Interoperability between wero and similar national schemes would be a good start.

A new survey found that about half of British adults are not familiar with the terms “Pay by Bank” or “account to account payments.” In fairness, a similar proportion hasn’t heard of Faster Payments either and that doesn’t stop people using the service. It’s all about the customer experience.

Klarna’s CEO has blasted open banking as a “failure.” His beef is that the APIs provided by the European retail banks “continue to be broken, lack functionality, and banks add as much friction as they can."

Whatever the quality of the underlying messaging, the market remains well supplied. The latest Konsentus tracker records 372 third party processors (TPP) in the EEA and 196 in the UK. TPPS’s are organisations with approval from one or more national regulators to provide open banking services.

Airlines are likely to be early adopters of open banking payments because they have a strong commercial interest in moving transactions away from cards. Edgar Dunn estimates that airlines pay $22bn each year in merchant service fees, 2.2% of total revenue. Those consumer credit guarantees are expensive! Consumers will need incentives to switch so it’s a smart move from Qatar Airways to offer 2.5 Avois per £ when paying by bank transfer. If you don’t mind transferring the money instantly and losing your consumer rights, this could be a good deal explains a points guru.

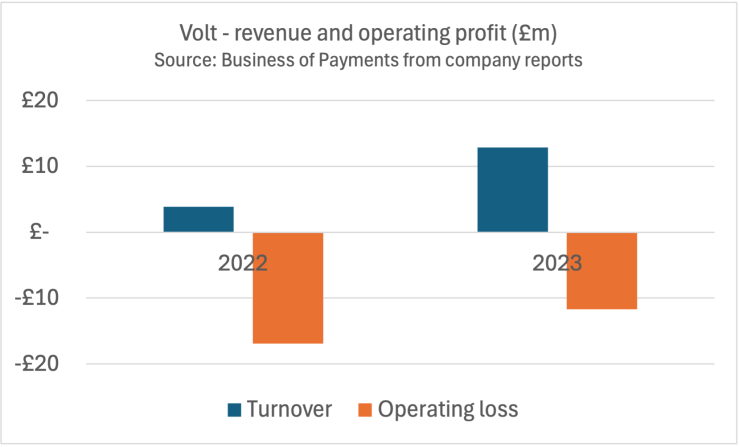

In vendor news, Volt, the self-styled “first global real-time payment network” recorded sales growing strongly in 2023 to £13m. Losses have narrowed. More details on the Business of Payments blog. Volt reports £1.46 revenue per transaction. This is higher than most competitors and indicates that Volt is focusing on high-margin sectors where pay by bank delivers significant value, such as gaming and crypto. In contrast, vendors trying to make a profitable business selling bank transfers to general retailers will likely struggle for some time yet.

Meanwhile, Banked, another London-based open banking vendor, reported an operating loss of £24m in 2023. Banked is active in Europe, USA and Australia. With a stellar investor list including NAB, Citibank and Raypd, Banked shouldn’t want for additional capital if needed.

Cash

As consumers shift to digital money, access to cash for those left behind is a growing political problem.

Only 3% of Norwegians use cash to pay for their shopping but the Government is introducing a new right to pay in cash for items up to 20,000Kr (€1,700). Retailers must give change “unless there is a clear discrepancy between the banknote offered as payment and the amount to be paid.” Iceland’s central bank is considering a similar measure and the Dutch parliament is deliberating an amendment to its anti-money laundering bill that would create an obligation to accept cash up to €3,000.

In Poland, the Commissioner for Human Rights has been asked to rule whether cashless parking meters discriminate against drivers without payment cards or mobile phones.

Cash has also entered into the German culture wars. According to Payment and Banking, the CDU party which won the recent elections is committed to the preservation of bank notes “because cash is lived freedom.” The opposition AfD agrees and wants to keep cash as a safeguard against “expropriation of [bank] account holders.” The SPD and FDP are in favour of an obligation to accept electronic money. The Greens are against “due to the high fees for traders.”

Crypto

The crypto industry is heading in two opposite directions. In one corner, Trump 2.0 is putting rocket boosters under the memecoin casino. In the other, stablecoins are ready to provide legitimate actors and criminals alike with tools to drive down the cost of remittances and facilitate new and (sometimes) useful products.

Stablecoins offer the technical benefits of crypto without the wild volatility. Fintech commentators are writing of little else. I’d recommend Matt Brown explaining how stablecoins work and Simon Taylor on the business case. His view is that stablecoins are not necessarily cheaper than cards or SWIFT messaging but could be better.

Stripe’s management is certainly very bullish about its acquisition of Bridge, a stable coin platform, although mainly for treasury management and payouts rather than consumer payments. But we’re also beginning to see stable coins in the wild popping up on the checkout pages of legitimate merchants although it’s not clear whether there’s yet much volume.

Criminals also like stable coins which accounted for 63% of illicit transactions in 2024, up from just 20% in 2020. Bitcoin, volatile and subject to high fees, is now only used for ransomware and darknet market sales, according to the FT.

Meanwhile, El Salvador has dealt a blow to the fiction that Bitcoin would ever be used as money, having ended its experiment with using this cryptocurrency as legal tender. Despite incentives and coercion, the public weren’t much interested. Crypto enthusiasts don’t spend their coins, they keep them in expectation of investment gains. Crypto sceptics avoid them. Nobody uses them to buy stuff.

In other news

Can you make a business case from payment data? Probably not. Payments data is no goldmine explains Andrew Dresner. I agree. If there was a pot of money to be found, someone would have discovered it by now.

Redsys is a beast. The Spanish bank-owned processor and gateway reported 2024 numbers showing €505bn payment volume from 1.5m connected POS terminals. With these economies of scale, you can see why it’s hard to beat Redsys on price.

Hat tip to Euronet for getting this ATM to the top of a mountain.

Klarna’s CEO says AI has allowed his business to stop hiring entirely. He expects the workforce to fall from a high of 5,000 to just 2,000. If every large business does this, the global economy will certainly be in trouble.

Wirecard latest. The trial of Markus Braun, the former CEO, still hasn’t finished and prosecutors are looking at ways of shortening what is becoming a very expensive process. Meanwhile, Jan Marsalek, Wirecard’s former COO, ran a Bulgarian spy-ring in the UK. The spies have gone to gaol, but Marsalek is still at large in Russia.

And finally

Nothing moves quickly in payments. Britain went decimal in 1971 having been thinking about the move since 1828. This newsreel explains how the government managed the changeover.

Where to find me

I’ll be at MPE 24 in Berlin this week, at the Retail Technology Show in London on 2/3 April and Money 20/20 in Amsterdam on 3/5 June.

Get in touch

Geoffrey Barraclough

geoff@barracloughandco.com